Drive Cardholder Loyalty with More Sustainable Options

The demand for more sustainable payment products is heating up. According to a November 2022 CPI survey conducted by an independent research firm*, 73% of

The demand for more sustainable payment products is heating up. According to a November 2022 CPI survey conducted by an independent research firm*, 73% of

In today’s fast-paced, lean environment, having a single-source provider to oversee every detail of your portfolio just makes business sense. In selecting that relationship, card

Today’s payment card environment is undoubtedly complex and competitive, but it pulses with possibility. Identifying a card program’s competitive edge is key to maintaining top-of-wallet

Smartphones are ever-present as we move through our day, and are rarely out-of-reach, so brands and advertisements persistently push phone-based interactions to deepen that customer connection: “text this number, scan this QR code, download our app,” etc. This poses a burning question:

Building a solid card program foundation starts with a thorough evaluation of both the financial institution’s needs as well as those of its cardholders to ensure the right mix of solutions for both.

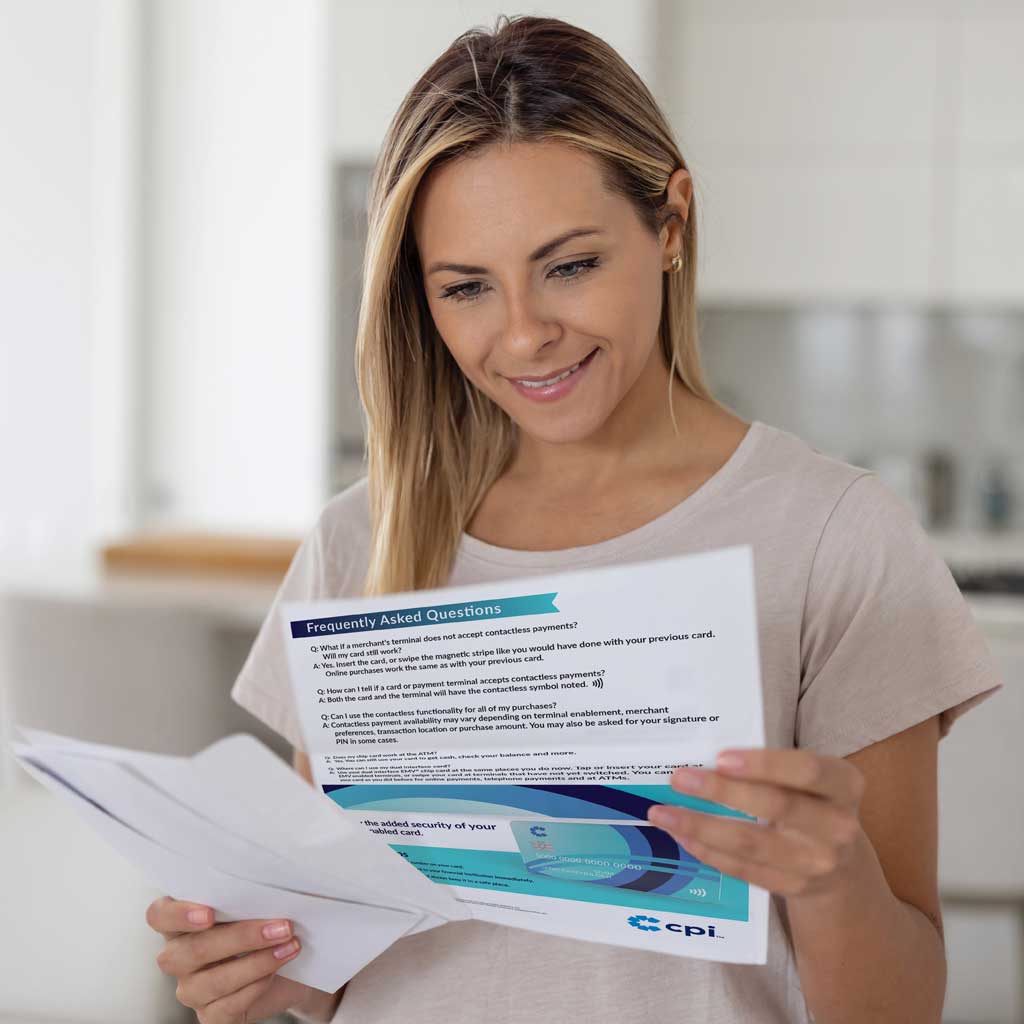

Extend your central and instant issuance strategy with a complementary digital payment solution to give cardholders the convenience and options they want. In February 2020,

What if you could make one change to your product offerings to potentially increase their activation and utilization, create a better customer experience, and simultaneously

Sustainability goals are influencing company identity and mission statements across industries, including the financial sector. Financial Institutions (FIs) of all sizes are setting sustainability goals,

Print-on-demand personalized payment card strategies offer a way for credit and debit card programs to stay timely and targeted in an individualized market. Personalization matters